We’ve tried to make it as easy as possible to manage your mortgage online. From making a payment to updating your information, you’ll find what you need here.

What are you looking to do?

See your mortgage information

Check your mortgage statement, see how much is left on your balance, or request a redemption statement here.

Make a change

Looking to move, change your mortgage, or update your details? See how to make changes to your mortgage here.

Make a payment

If you’re looking to make an overpayment or need to make a change to how you’re paying, you can do that here.

Money worries

If you’re feeling worried about money, we’re here to help. See what support we can offer to you.

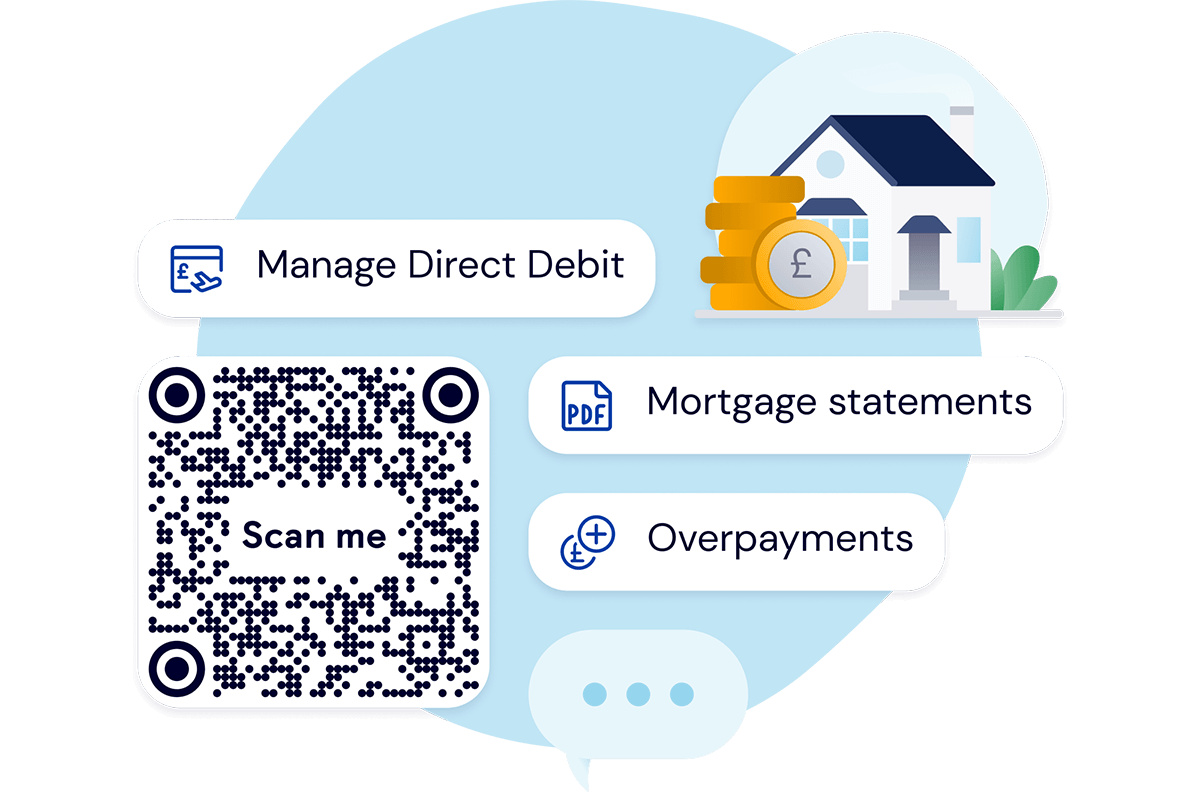

Manage your mortgage in the app

It’s full of tools to help manage your mortgage, from chatting to our Mortgage Experts, or simply viewing your balance.

Mortgage events

Want to learn more about the next steps for your mortgage? Our free, online mortgage events offer expert guidance that are tailored to where you are in the journey.

Snugg

A simple affordable way to make your home energy efficient. View your free personalised plan, check grants, find trusted installers and work out the best way to pay.

More mortgage help

Speak to an adviser

Want to talk about your options? Request a callback over video or the phone, or book a face-to-face appointment in branch.

Money worries

If you’re feeling worried about money or your mortgage, you’re not alone. We’re here to help.

Mortgage Charter

Set up by the FCA and the UK government, it offers customers more help and support with their mortgage repayments.